Labour leadership battle could push up UK bond yields

City economists and analysts are concerned that UK government borrowing costs could rise if the Labour Party holds a leadership race this summer.

UK bond yields could be pushed higher if investors fear an increase in borrowing under a Burnham administration, as the new MP for Makerfield pledges to address the cost of living crisis.

Dan Coatsworth, head of markets at AJ Bell, says there is potential for gilt yields to keep rising if Starmer “doesn't go quietlyâ€.

With 10 and 30-year bond yields higher today (in line with other European government bonds), Coatsworth says:

double quotation mark Friday's moves reflect the risk that Starmer won't go quietly. But they also reflect the setback with the US-Iran peace deal which has caused oil prices to rise again today, and inflation fears to remain on the table, thus having a direct read-across to interest rates and bond yields.“Over the coming days, the bond market will look for clues on Burnham's chances for getting the top job, and how he might steer Labour in a different direction. He might not have wanted to rock the boat ahead of the by-election for fear of causing upset or ruining his chances. Now he's in a stronger position to lay out policy changes and not simply tow the party line.

Reminder: Bond yields rise when the price of the bond falls, and are a gauge of the cost of issuing new debt.

This morning, the yield (or interest rate) on UK 30-year bonds is now up 8 basis points (0.08 of a percentage point) to 5.529%. That's only the highest since Tuesday, and some way below the 27-year high of 5.89% set in May, when borrowing costs were climbing.

Alexandros Xenofontos and Christopher Granville at City firm TS Lombard say gilts (UK government bonds) are constrained by the return of domestic political risk, explaining:

double quotation mark The question for gilts is whether the next Labour leadership preserves the Starmer-Reeves fiscal bastion, shifts left through funded tax-and-spend, or starts testing the fiscal rules.

Neil Wilson, investor strategist at Saxo UK, sees signs that markets are already worrying about the result from Makerfield, because:

double quotation mark a) the uncertainty that naturally surrounds a leadership race and b) more importantly, a likely crowning of Burnham as PM and leftwards lurch by the government as he is widely seen as the least market friendly option. I wouldn't be surprised if the multi-year/decade highs on the 10yr and 30yr are not tested again as he sets out his policy ideals.That said, however, the macro backdrop is different to early May when market angst over inflation was elevated and the market was pricing in multiple rate hikes by the BoE. The calculation relating to Hormuz and the BoE has changed markedly since then but the market will be hyper sensitive to how Burnham runs his campaign now.

There's also the scenario in which Burnham replaces Starmer, and calls a snap general election, to consider.

AJ Bell's Dan Coatsworth says that could really worry the bond market:

double quotation mark “Should an early general election be called and were Labour to lose power to Reform, then bond markets could have a much bigger issue on their hands.A Reform government would almost certainly make investors demand a higher reward for the risk of backing the UK, as Reform's policies are currently thin on detail. In that situation, expect higher bond yields, a more volatile pound, and concerns that any unfunded tax cuts will put even more pressure on government borrowing.â€

Key events

Closing post

Time to wrap up.

UK borrowing costs have risen today, amid a flurry of domestic and international factors.

The yield, or interest rate, on 10-year UK bonds is up 8 basis points (0.08 of a percentage point) at 4.78% this evening, with 30-year yields up 9bps to 5.535%. These aren't massive moves, but they do nudge the cost of borrowing higher.

UK bonds weakened amid speculation about whether Andy Burnham will replace Keir Starmer, having won the Makerfield by-election, and whether this would lead to higher borrowing to fund his plans.

They also dropped after the UK public finances showed a jump in borrowing in May, showing that whoever is prime minister faces a sticky fiscal situation.

The UK borrowed a higher-than-expected £23.3bn in May amid the economic fallout from the Iran war.

Bond yields were also pushed up by concerns that US-Iran talks planned for today in Switzerland to implement a peace deal were cancelled.

Analysts have warned that a summer leadership battle could push up UK borrowing costs.

Here are today's main stories:

We'll be back next week. Have a lovely weekend!

There probably isn't time for Andy Burnham to become prime minister and devise a large front-loaded fiscal loosening by the next Budget in the autumn.

Consultancy Oxford Economics's senior economist Edward Allenby explains:

double quotation mark “In part, this is because events have moved fast and there's little to suggest Burnham's team has a detailed policy package already in the works.“Developing that package in time for the autumn Budget will be made even harder if Burnham has to win a prolonged leadership contest first.â€

When it comes to the implications for the economy, a change in Prime Minister does not equal a change in fiscal realities.

So points out Ashley Webb, senior UK economist at Capital Economics, explaining to clients that the UK's weak fiscal position will constrain whoever is PM.

Webb explains:

double quotation mark That said, Burnham (or whoever becomes PM) could change both the size and composition of the state. He would probably be more interventionist than Starmer, with both higher spending and higher taxes. But his proposed tax hikes on the wealthy are unlikely to generate enough revenue to fully fund his planned spending increases, especially given the growing political pressure to increase defence spending.This suggests borrowing will be higher than on current plans and fiscal policy will be looser. Admittedly, Burham has rowed back on his comments that the government should not be “in hock to the bond markets†by reinforcing the need for “strong fiscal rulesâ€. So any increase in borrowing will probably be modest. And there will be a lot of talk and ink spilt over the coming weeks about which areas of public spending Burnham (or other possible leadership candidates) will want to raise, such as social housing construction, and which taxes could be raised to pay for it.

Eurasia Group, a consultancy, reckons there's an 80% probability that Keir Starmer will be replaced as prime minister, following Andy Burnham's strong victory in the Makerfield by-election.

Their managing director, Mujtaba Rahman, writes:

double quotation mark Despite Starmer's defiant mood, Eurasia Group believes an orderly transition of power by the Labour party conference on 27-30 September is more likely than a leadership contest; if Starmer sticks to his guns and forces a contest, Burnham will likely win it (an 80% probability).Burnham's allies will now try to convince Starmer to stand down, by demonstrating a show of strength among Labour backbenchers and mobilizing key Cabinet ministers Shabana Mahmood, Ed Miliband, Yvette Cooper and Lisa Nandy to put pressure on the PM to quit.

Ryanair’s O’Leary lands longer CEO contract

Lisa O'Carroll

In the airline sector, Michael O'Leary has had his contract as chief executive of Ryanair extended for another six years until 2032, by the company's board.

Concluding months of talks the board said he would continue on a “ modest annual salary and a capped annual bonus†along with a new one-off purchase option over 10m ordinary shares which can be cashed in at €26.70 – equal to the share price pre-Iran war.

But this is on condition that the company's pre tax profits reach over €4bn.

Last month, it was calculated that this bonus could be worth another €100m or more.

Ryanair chairman, Stan McCarthy said:

double quotation mark “As previously announced, this Spring the Board commenced discussions with MOL on his contract. I am pleased to report that this process, which included extensive engagement with Ryanair's largest shareholders, has successfully concluded with Michael agreeing to extend his leadership of the Ryanair Group for the next 6-years to April 2032, for the benefit of all shareholders.â€

UK National Drought Group meets after dry spring

As well as the possibility of nationalisation under a Burnham government, UK water companies are also facing the risk of a drought this year.

The National Drought Group met yesterday, and learned that some areas are already seeing the impacts of drier conditions.

Northern England receiving 90% of average rainfall in recent months compared to just 50% in Southern England, the Group says – which will counter the benefits of the exceptionally wet winter.

Worryingly, UK farmers have reported issues with the growth of spring crops and have had to begin irrigating earlier than normal because of the dry soils.

National Drought Group chair and director of water at the Environment Agency, Helen Wakeham, said:

double quotation mark We enter summer in a generally favourable position, but we can never be complacent ahead of those crucial drier months.Heatwaves will continue to be a concern as they can drive spikes in water demand, so we need to continue to work collaboratively to use our finite water wisely.

While many of us enjoy the hot weather, we ask everyone to be mindful of their water use. Every drop saved leaves more available for farmers, our local rivers and wildlife.

Back in the financial markets, the pound has bounced back from an early slide.

The pound hit an over two-month low of $1.3164 in early trading, but has now climbed back to $1.323, 0.2% higher on the day.

ONS reveals error with labour force survey data collection

Oh dear. The Office for National Statistics has just ‘fessed up to another error.

The ONS has admitted that it misallocated the telephone interviewers it uses to compile its labour force statistics, which means next month's unemployment data will be of lower quality than usual.

It accidentally allocated too many to its Transformed Labour Force Survey (TLFS), leaving too few collecting data for its traditional Labour Force Survey (LFS).

Both surveys are running in parallel, with the TLFS being created to tackle the problems getting enough people to respond to the LFS.

James Benford, director-general for surveys and economic and social statistics at the ONS (who was parachuted into the stats body to sort things out), says:

double quotation mark I am sorry that this issue occurred and regret that it was not detected and acted upon at an earlier point. Once the issue became clear, we undertook a number of rapid actions.Firstly, operationally, the issue has now been resolved. The measures we have put in place to ensure it doesn't happen again include tighter daily monitoring, reprioritisation of resource and changes to shift patterns and work allocation.

Next, we have been assessing how much impact this will have on our labour market statistics. In simple terms, there will be a level of reduced quality for our labour market statistics in July, with a smaller effect on the subsequent releases, because we will be replacing missing data points with estimated values.

British businesses are concerned that the UK could be dragged into a summer of speculation and drift, if Labour hold a leadership battle.

Rain Newton-Smith, CEO of the CBI, has warned:

double quotation mark The UK cannot afford a summer of speculation and drift while politicians are distracted by internal party dynamics. The government must remain focused on delivery and implementation.For strong, stable economic growth you need strong, stable, consistent government. Political uncertainty dampens business confidence and investment, impacting job creation, wages and the cost of living.

We need a government that is focused on the future, and getting on with the job of governing. Business needs to know that the government can take big decisions, will deliver on its commitments and is prepared to tackle the rising costs of doing business.

Small interest rate cut in Russia

Over in Moscow, Russia's central bank has cut interest rates… by less than expected.

At a time when some central banks are tightening policy (in Japan, and the eurozone), the Bank of Russia has trimmed its benchmark interest rate by 25 basis points to 14.25%.

That quarter-point rate cut is smaller than the half-point cut which analysts had expected.

Announcing the cut, the Bank of Russia warned that proinflationary risks still prevail over disinflationary ones on the mid-term horizon.

double quotation mark The proinflationary risks associated with high inflation expectations and a long period of wage growth outpacing productivity growth, as well as with a deterioration in the global economic outlook and rising global price pressures amid increased geopolitical tensions, are still in place.Proinflationary risks have increased due to a temporary decline in motor fuel production. Disinflationary risks involve a more significant slowdown in domestic demand.

Labour leadership battle could push up UK bond yields

City economists and analysts are concerned that UK government borrowing costs could rise if the Labour Party holds a leadership race this summer.

UK bond yields could be pushed higher if investors fear an increase in borrowing under a Burnham administration, as the new MP for Makerfield pledges to address the cost of living crisis.

Dan Coatsworth, head of markets at AJ Bell, says there is potential for gilt yields to keep rising if Starmer “doesn't go quietlyâ€.

With 10 and 30-year bond yields higher today (in line with other European government bonds), Coatsworth says:

double quotation mark Friday's moves reflect the risk that Starmer won't go quietly. But they also reflect the setback with the US-Iran peace deal which has caused oil prices to rise again today, and inflation fears to remain on the table, thus having a direct read-across to interest rates and bond yields.“Over the coming days, the bond market will look for clues on Burnham's chances for getting the top job, and how he might steer Labour in a different direction. He might not have wanted to rock the boat ahead of the by-election for fear of causing upset or ruining his chances. Now he's in a stronger position to lay out policy changes and not simply tow the party line.

Reminder: Bond yields rise when the price of the bond falls, and are a gauge of the cost of issuing new debt.

This morning, the yield (or interest rate) on UK 30-year bonds is now up 8 basis points (0.08 of a percentage point) to 5.529%. That's only the highest since Tuesday, and some way below the 27-year high of 5.89% set in May, when borrowing costs were climbing.

Alexandros Xenofontos and Christopher Granville at City firm TS Lombard say gilts (UK government bonds) are constrained by the return of domestic political risk, explaining:

double quotation mark The question for gilts is whether the next Labour leadership preserves the Starmer-Reeves fiscal bastion, shifts left through funded tax-and-spend, or starts testing the fiscal rules.

Neil Wilson, investor strategist at Saxo UK, sees signs that markets are already worrying about the result from Makerfield, because:

double quotation mark a) the uncertainty that naturally surrounds a leadership race and b) more importantly, a likely crowning of Burnham as PM and leftwards lurch by the government as he is widely seen as the least market friendly option. I wouldn't be surprised if the multi-year/decade highs on the 10yr and 30yr are not tested again as he sets out his policy ideals.That said, however, the macro backdrop is different to early May when market angst over inflation was elevated and the market was pricing in multiple rate hikes by the BoE. The calculation relating to Hormuz and the BoE has changed markedly since then but the market will be hyper sensitive to how Burnham runs his campaign now.

There's also the scenario in which Burnham replaces Starmer, and calls a snap general election, to consider.

AJ Bell's Dan Coatsworth says that could really worry the bond market:

double quotation mark “Should an early general election be called and were Labour to lose power to Reform, then bond markets could have a much bigger issue on their hands.A Reform government would almost certainly make investors demand a higher reward for the risk of backing the UK, as Reform's policies are currently thin on detail. In that situation, expect higher bond yields, a more volatile pound, and concerns that any unfunded tax cuts will put even more pressure on government borrowing.â€

The rise in UK bond yields, because of political uncertainty, will be nervously watched by the Bank of England's monetary policy committee (MPC) as it represents a tightening of financial conditions, Professor Costas Milas of the Management School at the University of Liverpool tells us.

Rising bond yields will put the spotlight on the Bank's quantitative tightening (QT) programme, in which it is selling off the government bonds it bought after the financial crisis and during the Covid-19 pandemic. Selling bonds puts upward pressure on bond yields.

Professor Milas says:

double quotation mark The rise in yields, if it continues, will surely raise the issue of whether the MPC should halt or even reverse its QT policies. It should NOT for two reasons: First, the MPC shouldn't intervene with Labour's political infighting and consequent turbulence.Second, in a recent BoE Working Paper, colleagues and I show that QT policies have reduced CPI inflation by 1.4 percentage points compared to the case where QT policies were not pursued. In other words, and this is strictly my personal opinion, the MPC should continue with QT as normal because it puts a “lid†on inflation pressures.

Asda slumps to near £1bn loss

Sarah Butler

British supermarket group Asda slumped to a near £1bn loss last year after it kicked off a supermarket price war and revamped its IT systems.

Sales, including fuel, fell 3.6% to £25.9bn – including a 3.1% drop at established stores – but losses widened from £599m in 2024 to £989m after Allan Leighton, the executive chairman of Asda last year pledged to invest “a pretty significant war chest†in cutting prices and putting more staff on the shop floor.

His aim is to make Asda, which has 580 supermarkets, 517 convenience stores and four stand-alone outlets for its George clothing and homewares brand, 5% to 10% cheaper than its traditional rivals – Tesco, Sainsbury's and Morrisons – and are now between 4% and 7% cheaper.

An Asda spokesperson said:

double quotation mark Asda invested significantly to lower prices for customers in 2025 and strengthen its value proposition at a time of sustained cost of living pressures.

Leighton has said it could take up to five years to turn around Asda, which is at risk of losing its spot as the UK's third largest supermarket to German-owned discounter Aldi.

Leighton, who returned to lead the business in November 2024 after a 20-year absence, has said availability has improved dramatically now most of the IT problems have been fixed and a new deal with Ocado will help modernise Asda's currently declining online business from next year.

There are also plans to expand the George brand with more standalone stores and better presentation in Asda's supermarkets.

The figures, which have been filed at Companies House today, show the loss also comes after £656m of one-off costs including £284m related to Project Future, the IT separation from Walmart, and a £344m impairment on Asda's £8bn property portfolio.

The latest update takes the total spent on Project Future to about £1.2bn, with Leighton recently admitting there was still some more work to do.

The Asda spokesperson said:

double quotation mark The reported loss does not reflect the underlying financial strength of the business – and continued powerful cash generation.Asda is supported by a strong balance sheet and capital structure, with £1.3bn in cash, £2.1bn of total liquidity at the year end, and the majority of borrowings secured well into the next decade. This gives us the flexibility to continue investing in our long-term growth strategy and deliver a disciplined and sustainable turnaround.

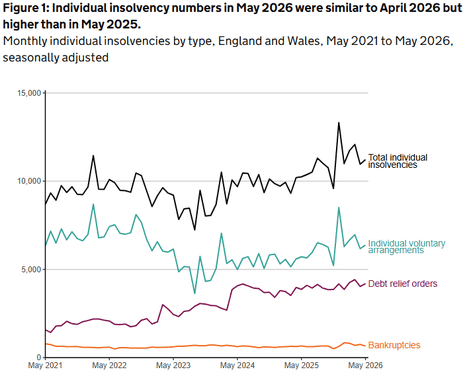

Personal insolvencies rise in England and Wales

There's mixed news from the latest insolvency data.

The good news is that the number of registered company insolvencies in England and Wales fell by 10% month-on-month in May, to 1,868, thanks to a drop in liquidations and administrations.

That's 16% lower than in May 2025.

However, the personal insolvency data paints a worse picture; 11,223 individuals entered insolvency in England and Wales. That's 10% higher than in May 2025, and little changed month-on-month.

For markets, the key question following the Makerfield byelection is whether this political shift translates into a change in the policy framework, explains Modupe Adegbembo, economist at the investment bank Jefferies.

That's because the binding constraint on the government is not ideology but fiscal space and execution capacity, Adegbembo explains:

double quotation mark Under Burnham, his comments suggest the overarching macro framework would be largely unchanged. He has committed to existing fiscal rules and manifesto tax constraints, underscoring the limited room for policy easing. At the same time, he has provided little indication that he would seek to reduce public spending, having already pledged to keep the pension triple lock and, at times, signalling support for policies with a significant fiscal cost, such as compensation for WASPI women (though he later ruled out compensation). While he has shown some willingness to adjust policies, we continue to think the thrust of policy remains constrained by the fiscal backdrop.The key shift is likely in political emphasis, with greater weight on the soft-left and Burnham's “Manchesterismâ€, rather than a material loosening of the framework. “Manchesterism†looks less about fiscal expansion and more about place-based partnerships with the private sector, alongside greater use of regulatory levers, sector oversight and procurement to deliver policy at the margin. This is a shift investors may be underestimating.

Bank of England to test how private credit would handle a 1970s-style economic crisis

Kalyeena Makortoff

The private credit and private equity industries will reveal how they would respond to a “severe but plausible†economic shock involving surging inflation, a 30% drop in key stock markets, and major disruption to the booming AI sector, as part of a world-first test unveiled by the Bank of England.

The stress test scenario, released this morning, covers a global shock lasting five years, starting with a surge in geopolitical tensions that leads to fragmented global trade and supply chains. Jitters filter through, leading to CPI inflation of 7%, a hike in borrowing costs and trigger 30% declines in the FTSE All Share Index and a 35% drop in the S&P 500 within the first year.

In this scenario the UK suffers a 1970s style economic crisis, marked by a sharp drop in trade and hike in import costs, hitting company revenues. Tech, consumer discretionary and industrial sectors are hardest hit, though the BoE has made sure to outline specific impacts to the AI sector, which has been fuelled by private credit investments.

It says:

double quotation mark Expectations of future disruption from artificial intelligence (AI) weigh on valuations in software and services sectors, particularly in companies judged as having weaker competitive advantages or a ‘smaller moat' as a result of AI. Disruption to supply chains and weaker demand also weighs heavily on hardware.At the same time, AI-development is hit by higher energy prices and a shortage of key hardware components. This increases the costs for users of AI and slows the development of new models, meaning the near-term productivity gains from AI are limited.

The stress test is meant to map out potential risks linked to the private market boom, including whether the private credit and private equity sectors could end up amplifying financial and economic shocks.

It's a first step towards understanding how influential private markets become within the financial system, having long been criticised for a lack of transparency.

It will be quite an involved process, with results due to be released to the public in early 2027.

Burnham’s ‘Manchesterism’ is already reshaping Labour's debate

Investment bank Cavendish argues that Andy Burnham is already reshaping the government agenda.

In a new report after the Makerfield byelection, Cavendish point out that this is particularly important for water and transport companies, saying:

double quotation mark The agenda arrives before the man. This is the part that matters even if Burnham never reaches No 10. His platform – “Manchesterism†– is already reshaping Labour's debate, and the soft-left network behind it is ascendant regardless of the result.It names specific sectors and sets out to change the terms on which they operate: increased scrutiny of tech, greater public control of energy, the sharpest exposure of all in water, bus and rail franchising in transport, a for-profit care model it wants to dismantle, and around £40bn of borrowing to build.

Any organisation in or near those sectors is already inside the policy, whether it has noticed or not.

UK two-year gilt yield rises to one-week high after by-election and borrowing data

A week is a long time in politics, and also in the bond markets!

Reuters has spotted that short-term British government bond yields have risen â to a one-week high on Friday, increasing â slightly more â than those ​for German debt, after this morning's higher-than-expected borrowing numbers and an â election victory for Greater Manchester Mayor Andy Burnham.

Two-year gilt â yields rose to their highest ​since June 12 ‌at 4.25%, up more ‌than 6 basis points on the day and rising around 2 bps more than equivalent German bonds.

{kind=link}